Homeownership is a life-changing event. So is having a large amount of debt. Whether you own a home or are planning to buy one, knowing your options for managing your debt is crucial.

If you’re struggling to make monthly payments on your debt, you may be investigating different debt relief options to get rid of that debt so you can have enough leeway to make mortgage payments. Filing for bankruptcy makes it incredibly difficult to qualify for a mortgage. So, instead of bankruptcy, you might be considering debt consolidation.

Here’s the critical question: does debt consolidation affect your home-buying ability? Below, we will review how debt consolidation works, how it can affect buying a home, and some strategies for balancing your debt management with your mortgage.

Understanding Debt Consolidation

Debt consolidation is a blanket term for a variety of strategies that combine multiple forms of debt into a single monthly payment. There are three major strategies to consider: debt consolidation programs, debt consolidation loans, and rolling debt into your mortgage.

Each of these strategies can impact your credit score and ability to buy a home or maintain your existing mortgage.

About Debt Consolidation Programs

A debt consolidation program (DCP) is when you work with a certified credit counsellor to negotiate with your creditors to reduce (or even eliminate) the interest on your debt. Then, you make a single monthly payment to your credit counselling agency, which then redistributes payments to your creditors.

It should be noted that a DCP can only cover unsecured debts. Secured debts with some form of collateral, such as a car loan, cannot be included in the program.

While on a DCP, your creditors may apply an R7 rating to your credit report for the duration of the program plus two years after the program is complete. Also, you will be required to surrender any unsecured credit cards as a part of the program.

About Debt Consolidation Loans

A debt consolidation loan is when you apply for a personal loan to get the money you need to pay off your existing debts. You then start repaying the loan instead of the high-interest credit cards, outstanding bills, and other debts that you’ve paid off.

The benefits of a debt consolidation loan include an overall lower interest rate on your debt and, if you make payments on time, helping you improve your credit score.

However, you need to get approved for the loan. This might be difficult if you have a low credit score. If you don’t have a good credit score, you might get offered loans with higher interest rates than the debt you already hold. On the other hand, some loans might require you to secure them with collateral that the lender can claim if you fall behind on your repayment schedule.

About Rolling Debt into a Mortgage

If you already have a home, a third option is to roll your debt into your mortgage. Sometimes called a “debt consolidation mortgage,” this is a debt consolidation strategy that leverages your home equity (the difference between how much your home is worth and how much you owe on it) to repay your debts. However, this isn’t just for existing homeowners—prospective buyers can also apply for a mortgage larger than they need to purchase the home and use the extra money to pay off their high-interest credit card debt and other bills.

One of the biggest advantages of consolidating debt into your mortgage is reducing the interest on your debt even more than with an unsecured loan. Why is this? Mortgages tend to have lower interest rates than unsecured loans because the mortgage is secured with collateral, and the unsecured loan is not.

However, to consolidate your debt into your mortgage, you need to have enough equity in your home to cover the debt and pay fees for breaking your existing mortgage agreement. If you’re rolling your debt into a brand-new mortgage, then the biggest obstacle may be qualifying for a mortgage that covers both the cost of your new home and your outstanding debt.

Additionally, this form of debt consolidation means delaying paying off your home in full as you add to the mortgage’s principal balance (i.e., the amount of money owed that isn’t interest) or if the interest rate and terms of the mortgage are changed.

Debt to Income Ratio and Buying a Home

When you’re applying for a mortgage, the mortgage company will want to examine your debt-to-income ratio or DTI. Typically, a lender will want a borrower to have a back-end DTI of 35% or less. However, some lenders may have stricter DTI guidelines or accept borrowers with a higher DTI.

This is one reason why debt consolidation can be essential for buying a home. By consolidating debts in a way that lowers your interest rate (or completing a DCP and eliminating your debts), you can reduce your DTI and make qualifying for a mortgage easier.

What Is Debt to Income Ratio and How Is It Calculated?

The debt-to-income ratio allows lenders to compare how much of a borrower’s monthly income is being put towards monthly debt payments.

For example, if you made $10,000 a month and had to spend $3,000 on debt payments, your DTI would be 30%.

Some borrowers might specify a difference between “front-end” DTI (which only covers housing expenses) and “back-end” DTI (which includes all debt obligations).

Debt Consolidation and Home Buying

So, does debt consolidation affect buying a home? The answer depends on the type of debt consolidation you use because each form of consolidation has a different impact on your credit.

Debt Consolidation Programs and Buying a Home

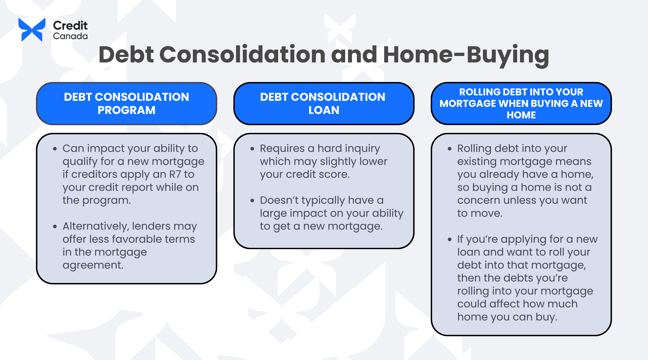

A debt consolidation program can impact your ability to qualify for a new mortgage. This is because creditors may apply an R7 rating to your credit report while on the program (some creditors may apply different ratings, but R7 is the most common). When this happens, lenders may see the item on your credit history and decide not to work with you since the rating indicates an account where you have made an alternative arrangement to repay your creditors.

Alternatively, they may offer less favourable terms in the mortgage agreement. This includes things like charging a higher interest rate or reducing how much you can borrow. This can make it more difficult to buy the home that you want.

Debt Consolidation Loans and Buying a Home

A debt consolidation loan doesn’t typically have a large impact on your ability to get a new mortgage. While the hard inquiry on your credit report can have a negative impact on your score, credit inquiries only account for 10% of your credit score. This is less impactful than items like your payment history, which accounts for 35% of your score, and credit utilization ratio, which accounts for 30% of your credit score.

In fact, by making consistent monthly payments on the consolidation loan on time, you can build a positive credit history and improve your credit score—making it easier to qualify for a mortgage over time.

Rolling Debt into Your Mortgage When Buying a New Home

If you’re rolling debt into your existing mortgage, you already have a home, so buying a home is probably not a concern unless you want to move. However, if you’re applying for a new loan and want to roll your debt into that mortgage, then the debts you’re rolling into your mortgage could affect how much home you can buy.

It’s a good debt management strategy to spend even less on your home than the mortgage value you qualify for. This is because taking a smaller loan than what you’re approved for can help you pay off your mortgage even faster and help you put aside more money for the future since you’re not paying as much interest on the mortgage.

Strategies for Balancing Debt Consolidation and Home Purchase Goals

So, how can you balance the need to manage your debt with your goal of purchasing a new home (or paying off your mortgage)? Some strategies for minimizing the impact of debt consolidation on your goal of buying a home include:

Leveraging a Debt Consolidation Loan

Consider applying for a debt consolidation loan as a first option for clearing your outstanding debt. While the hard inquiry has a small impact on your credit score, the steady repayment of your loan can help you build a positive history and improve your credit score.

Reduce your interest rates and make your debt easier to manage. Learn more about our Debt Consolidation Program today.

Don’t Buy More Home Than You Can Afford

How much can you afford to spend on your mortgage every month? Before setting out to get a mortgage for a new home, take some time to create a monthly budget so you can track your income and expenses.

How much are you spending on necessities like food or rent? How much money do you currently spend on rent? Can you set aside enough money to cover your monthly minimums on debt payments? What expenses could you cut back on, if necessary?

Using a budget planner tool can help you clearly establish how much you can afford for your monthly payment.

Create a budget that works for you. Use our Free Budget Planner to get started on your path to financial stability. Get Your Budget Template today.

Consider Paying Off High-Interest Debts Before Buying a Home

If you cannot secure a debt consolidation loan or roll your debts into your new mortgage, consider focusing on your debts with the highest interest rates before applying for a mortgage.

By making larger, regular payments against your highest interest debts while maintaining the minimum payments on other debts, you do two things to help you improve your credit score:

- You create a positive history of making on-time payments; and

- You improve your credit utilization ratio.

These are both major factors that affect your credit score.

Make a list of your debts, the total amount you owe, and the interest rates for each form of debt you hold so you can identify the most important debts to repay first.

Set Aside Extra Money for Your Down Payment

If you’ve cleared your high-interest debts (like credit cards) and still can’t find a home that is affordable for you, consider setting aside more money for your down payment. Saving up money to make a larger down payment means you will need a smaller mortgage loan when making a purchase—making it easier to buy your dream home.

Additionally, it can serve as an emergency fund while you wait for the prime rate (the interest rate that banks charge their best customers) to improve. This can help you cover emergency expenses without going into more debt.

What’s the Best Option for You? Reach Out to a Certified Credit Counsellor for Advice!

The impact of debt consolidation on your ability to buy a home can vary depending on the consolidation method that works best for you. If you have good credit, you should try to get a debt consolidation loan or roll your debts into your mortgage, as these methods have a small impact on your credit score.

In the case of a debt consolidation loan, securing the loan and then consistently making payments on it can help you improve your credit score to get a better mortgage.

A debt consolidation program is a good alternative for those who don’t have great credit and need an opportunity to clear their unsecured debts so they can start building a positive credit history. If you join a DCP, consider waiting for at least two years after the program ends before applying for a mortgage.