Frequently Asked Questions

Have questions? We are here to help.

If your financial situation has progressed to the point where you’re considering bankruptcy or debt consolidation, it’s important to know about your options and what you can do to find debt relief. When weighing debt consolidation vs bankruptcy, it can help to know the basics about each: what they are, how they can impact your credit score, and which option would be best for your long-term financial health.

Let’s discuss debt consolidation and bankruptcy, their pros and cons, and what you can do to improve your financial situation moving forward.

Debt consolidation is the practice of taking multiple sources of debt and combining (i.e., consolidating) them into a single monthly payment. This helps make it easier to keep track of debt payments and creditors.

There are several options for consolidating debt. For example:

Different debt consolidation options will fit different needs. For example, if you have an excellent credit score, you might want to pursue a debt consolidation loan because you may be able to get a lower interest rate, improve your credit utilization ratio (the amount of credit you’re using compared to the amount of credit available to you), and simplify your debt repayment schedule. However, such a loan would also generate a hard inquiry against your credit and open a new line item on your credit report—temporarily impacting your credit score.

On the other hand, if your credit score is lower and you cannot secure a debt consolidation loan, a debt consolidation program might be the better alternative. Credit Canada has years of experience in guiding Canadians on the path to being debt-free through credit counselling and DCPs.

Bankruptcy is a legal process administered by a Licensed Insolvency Trustee (LIT) like Spergel. Under a bankruptcy declaration, you would surrender your assets (minus those that are exempt) to the LIT, who would then be charged to sell them off to repay your creditors.

At the end of the process, the goal is to receive a bankruptcy discharge which would release you from most forms of debt. Some forms of debt cannot be discharged through a bankruptcy filing. For example, secured debts such as mortgages are not discharged through bankruptcy as bankruptcies do not affect the rights of secured creditors. Also, child support and alimony payments are similarly excluded from bankruptcy discharges.

Student loan debt is a bit of a unique case. If you were a full or part-time student within the last seven years, student loan debt cannot be discharged in a bankruptcy. However, after seven years of no longer being a student, then the student loan could be discharged through a bankruptcy filing—though the determination of when you ceased being a student may be calculated differently depending on the rules for your province. Also, this time restriction may be reduced to five years instead if repaying the loan would result in undue hardship.

Bankruptcies have a strong impact on your credit score. After filing for bankruptcy, your credit rating will be set to the lowest possible level (R9). A credit rating is a kind of shorthand that lenders use to describe your debt repayment habits and an R9 rating indicates that you have bad debt, debt placed in collections, or a bankruptcy. This rating will remain until the information is removed from your credit report. This can take six or seven years for a first-time bankruptcy filing and 14 years for subsequent filings.

The credit impact of filing for bankruptcy means that it should be the debt relief option of last resort. According to data from the Government of Canada, in Q3 of 2023, there were 24,043 consumer proposals and 6,428 bankruptcies filed in Canada by consumers, for a total of 30,471 insolvency filings. A consumer proposal is an arrangement between debtors and creditors to alter their repayment terms and is a common alternative to bankruptcy that has a lesser impact on a consumer’s credit score.

The process begins with you reaching out to a Licensed Insolvency Trustee. They will review your application and decide whether to accept your file. If you cannot find an LIT to accept your file or cannot afford the LIT’s services, you may be able to get help through the Office of the Superintendent of Bankruptcy’s (OSB’s) Bankruptcy Assistance Program—assuming you meet criteria such as having already reached out to two LITs, not being involved in commercial activities, not being required to make surplus income payments*, and not being currently in jail.

*Note: Surplus income is income above the amount needed to maintain a reasonable standard of living. If your LIT determines that you make surplus income in excess of $200, you will be required to make additional payments to the LIT to repay your creditors.

When you find an LIT, they will work with you to file the required forms and submit documents to the OSB. Once you have been declared bankrupt:

At the conclusion of the bankruptcy, you will receive a bankruptcy discharge. A bankruptcy discharge is the release from your debts that you had at the time you filed for bankruptcy (some exceptions apply). Discharges can be automatic if:

For a first-time filer who does not need to make surplus income payments, an automatic discharge from bankruptcy occurs after nine months. First-time filers who do need to make surplus income payments can be discharged after 21 months.

On a second bankruptcy, the time to automatic discharge increases to 24 months for those who don’t need to make surplus income payments and 36 months for those who do.

If you don’t qualify for an automatic discharge, you will need to go through a discharge hearing with the court. The LIT will arrange for this hearing and prepare a report for the court. Note that the court may choose to refuse your bankruptcy discharge. If this happens, contact your LIT and they will inform you of the reason for the refusal and what your options from there may be.

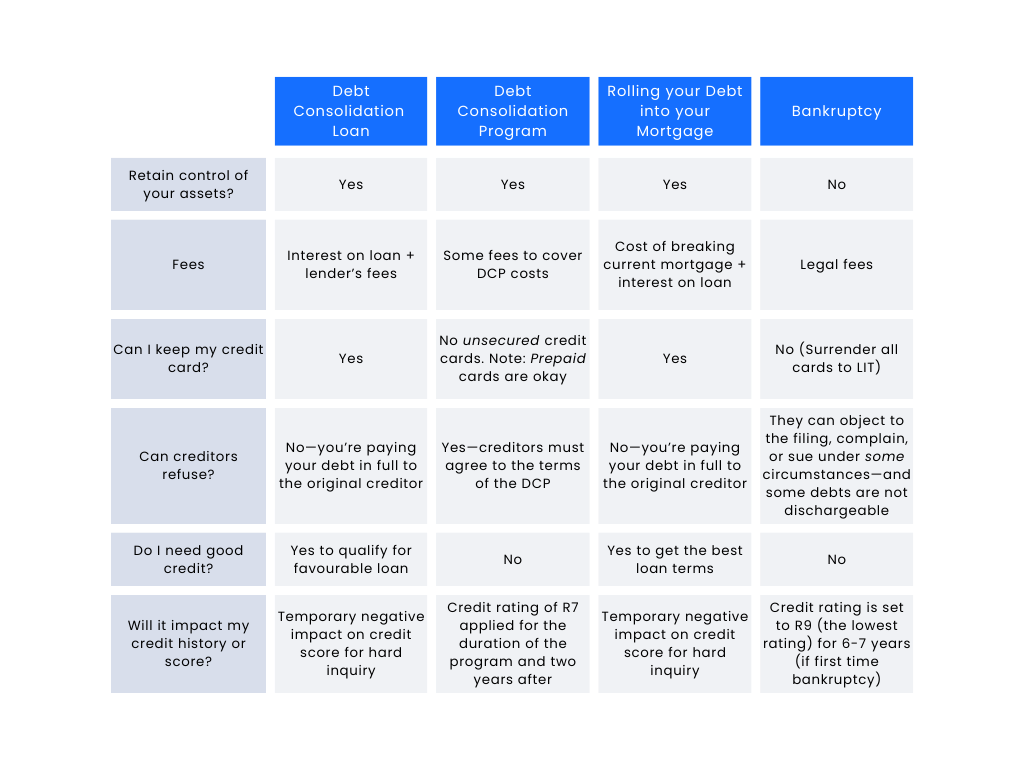

Debt consolidation and bankruptcy are very different processes that have different impacts on your financial solution, but both can be viable paths to debt relief for those who find that their monthly payments for debt are outpacing their ability to afford them.

But which one is right for you? Let’s weigh the pros and cons of debt consolidation vs bankruptcy:

All of these options have the benefits of stopping nuisance collection calls and, when completed successfully, leaving you debt-free.

Of these processes, bankruptcy has the largest impact on your credit as the bankruptcy filing will remain on your credit history for six to seven years for a first-time filing and 14 years for each subsequent filing. Also, the discharge from bankruptcy is not guaranteed, so ask the LIT or your financial advisor for advice before beginning the process.

Meanwhile, a debt consolidation program has a lesser impact on your credit history and score than bankruptcy. Also, the R7 rating fades from your history more quickly than the R9 rating applied by bankruptcy.

Debt consolidation loans or rolling debt into your mortgage has the smallest impact on your credit score in the long term as these actions affect your utilization ratio and produce a hard inquiry, but also help you build your credit history afterward.

So, which is best for you? Debt consolidation or bankruptcy? The answer is: it depends on your financial situation.

A debt consolidation loan might be best if:

Rolling your debt into your mortgage might be a good idea if:

A debt consolidation program can be ideal if:

Filing for bankruptcy may be the best option if:

Choosing between debt consolidation and bankruptcy should not be taken lightly. If you’re examining these options, it’s important to seek help and advice from someone with expert knowledge.

This is where a Certified Credit Counsellor can help. A credit counsellor can help you review your financial situation and examine your debt relief options to choose the best path forward for your long-term financial health. They can help you sort the myths from the facts when it comes to debt management and repayment so you can make a more informed decision.

When you’re done with your bankruptcy filing or used debt consolidation, what’s next? The road to recovery can be a long one, but following some good money habits can help you improve your financial situation moving forward and build your credit score back up over time.

It won’t be easy. It won’t be fast. But, with consistent effort, you can do it. Some basic tips include: