.png?width=128&height=128&name=Untitled%20design%20(26).png)

Frequently Asked Questions

Have questions? We are here to help.

Becoming debt-free is a major goal for many Canadians. Paying off your debts is liberating and makes it easier to achieve your other financial goals—like home ownership, starting your own business, or retirement.

However, amid the rising cost of living and the occasional emergency expense, it can be difficult to make progress on your goal of being debt-free.

Credit Canada has created a free debt repayment spreadsheet to help you get out of debt. This spreadsheet will help you understand your total debt and track your progress towards becoming debt-free.

Get Help Tracking Your Progress Toward Being Debt-Free. Download the Debt Repayment Spreadsheet.

Before you begin using the spreadsheet, you’ll need to assemble a few key pieces of information, such as your estimated monthly income and details about your debt.

Debt amounts

Interest rates (if applicable)

Debt payment due dates

Minimum payment amounts for each debt

Repayment plan details

Creditors for each debt

Estimated payoff dates (if available)

Assembling information about your debts will help you fill out the repayment spreadsheet and better understand how close you are to meeting your goal. This information is also useful for prioritizing which debts to focus on repaying first.

Where can you find this information? For most debts, you can find this information in the statement from your creditor. If you cannot find your statement, contact your creditor and request a copy of your statement. It can also help to record the creditor’s contact information into the spreadsheet.

You can also check your credit report to verify debts on your record. In any case, you should check your credit report for any unfamiliar debts that you may need to dispute.

Download the Debt Repayment Spreadsheet document and save it to your computer or mobile device. This is a Google spreadsheet that you can copy to your Google Drive or download.

For each debt you have, add its information to the repayment spreadsheet. Be sure to clearly label each debt and double-check the data for each debt.

Determine which debts are the most important to pay off first. A common strategy is to prioritize the debts with the highest interest rates to pay them off first while paying the minimum amounts for every other debt. (More details on this strategy later).

This is the fun part! At the end of each month, go into the tab for the next month and enter the updated information for each of your debts. Repeat this process at the end of each month until you’ve paid off all of your debts.

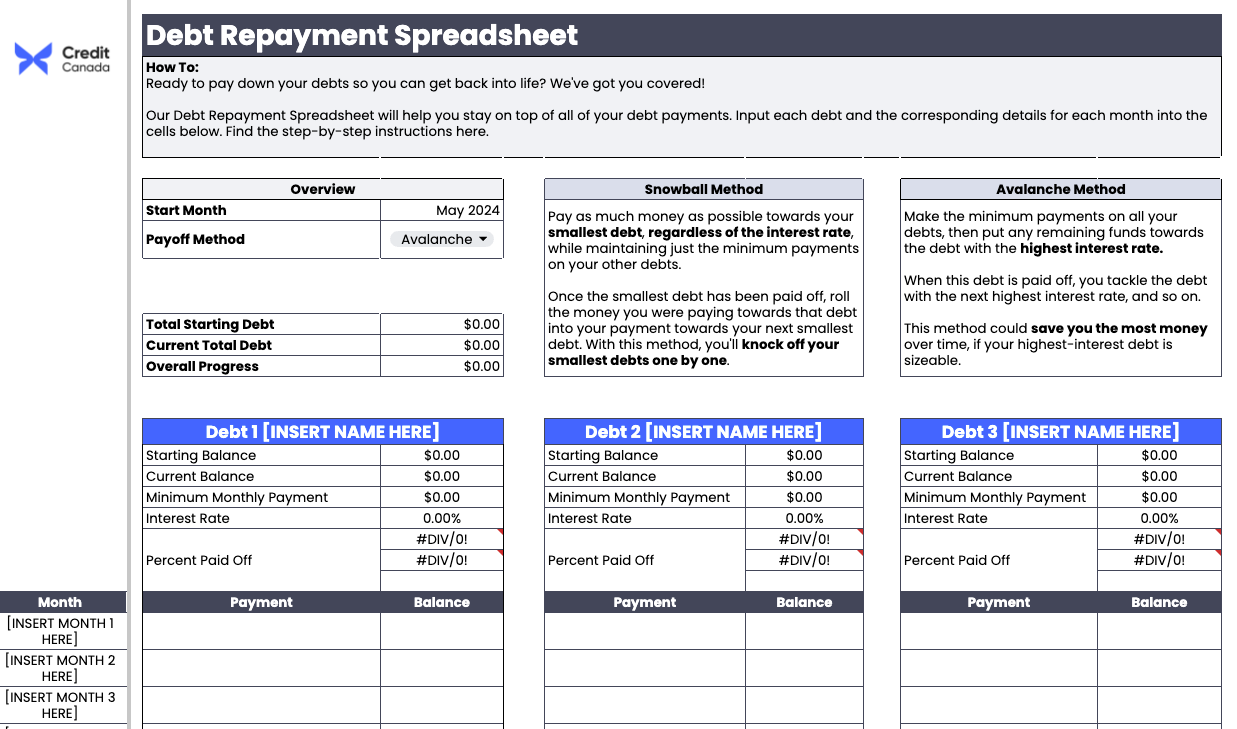

Here’s a screenshot showing the debt repayment spreadsheet:

Get a tutorial on how to use this spreadsheet to track your debt repayment and meet your goal of becoming debt-free by clicking this link. Here’s a breakdown of how to use the spreadsheet:

In the “overview” box, enter the current month in the cell next to the “Start Month” cell.

Choose a payoff method from the dropdown menu—avalanche or snowball (you can find information about each of these methods in the spreadsheet and in the next section of this article).

Add up all of your debts to determine your total starting balance.

In the following months, you can subtract your current total debt from your starting debt to determine your overall progress. For example, if you start with $25k debt and pay it down to $20k debt, you will have made $5k of progress.

In each of the sections with the blue “INSERT NAME HERE” bars, name each of your debts and enter information specific to each—starting balance, current balance, minimum monthly payment amount, and interest rate (if applicable).

In the “Month” section, replace the “Month 1” text with the current month and year (for example, August 2024), next month in “Month 2,” and so on.

Each month, log the amount you paid on each debt and track your current balance. Repeat this process for each row of the spreadsheet. When you update your current balance, you’ll see that the “Percent paid off” section will update automatically.

The graph in the upper-right of the spreadsheet provides a visual of your overall progress toward paying your debt to help you stay motivated and on track.

When you’re working on repaying your debts, you need to select a strategy that suits your situation and that you are confident that you can stick to. This helps you meet your debt repayment goal by keeping you focused. Two strategies to consider are the avalanche and the snowball methods of debt repayment.

Avalanche Debt Repayment. Here, you put all of your extra payments to the debt with the highest interest rate until it’s paid off while only paying the minimum on other debts. Once a debt is paid off, you roll any extra payments that were going to it into the next-highest-rate debt—repeating until all debts are paid. This method tends to save the most money in the long run because it eliminates high-interest debts first.

Snowball Debt Repayment. This is when you focus on the smallest debts first and then roll extra payments into the next debt once the smallest debt has been paid off. Many find it easier to stay motivated to pay off debts under this strategy since they see debts being eliminated faster than with the avalanche method.

Use Windfalls to Pay Down Debts. If you receive a financial windfall like an inheritance or a tax refund, consider putting that extra money towards paying off your highest-interest debt. This can help you save money on interest, get you out of debt faster, and put you in a better position to meet your financial goals later.

Switch to Prepaid or Debit Cards. Using prepaid credit cards instead of traditional credit cards can help you avoid paying interest and keep to your budget for your shopping since you can only spend what’s available on the card. Many banks also offer debit cards with credit logos that can be processed like a credit card but take the money out of your chequing account.

"If you are dealing with debt, managing it head-on is always the best course of action. Ignoring it or sweeping it under the rug will only worsen things in the long run."

Mike Bergeron, Counsellor Manager, Credit Canada

As you make progress on paying off your debt, plan to regularly assess and adjust your debt repayment plan. Update your debt repayment spreadsheet each month to see your progress and change how you allocate your funds if needed.

For example, say that your mortgage is up for renegotiation and the terms change to make your monthly payment different. You would then need to rebalance your debt payments to account for that change. However, a mortgage negotiation might also be a good opportunity to take advantage of the equity in your home to roll your high-interest debts into your mortgage.

If you need information and advice about using the debt repayment spreadsheet or getting out of debt, reach out to the certified credit counsellors at Credit Canada. Our counsellors have helped thousands of people get out of debt and stay debt-free afterwards.

You don’t have to face the challenges of debt repayment alone. With resources like the free debt repayment spreadsheet and credit counselling, there is a path to becoming debt-free.